Owning a home is perhaps the most significant milestone for any family in Pakistan. However, with the rising costs of construction and real estate, many feel that this dream is slipping out of reach. If you are tired of paying monthly rent and want to invest that money into your own walls and roof, there is a specialized solution available right now.

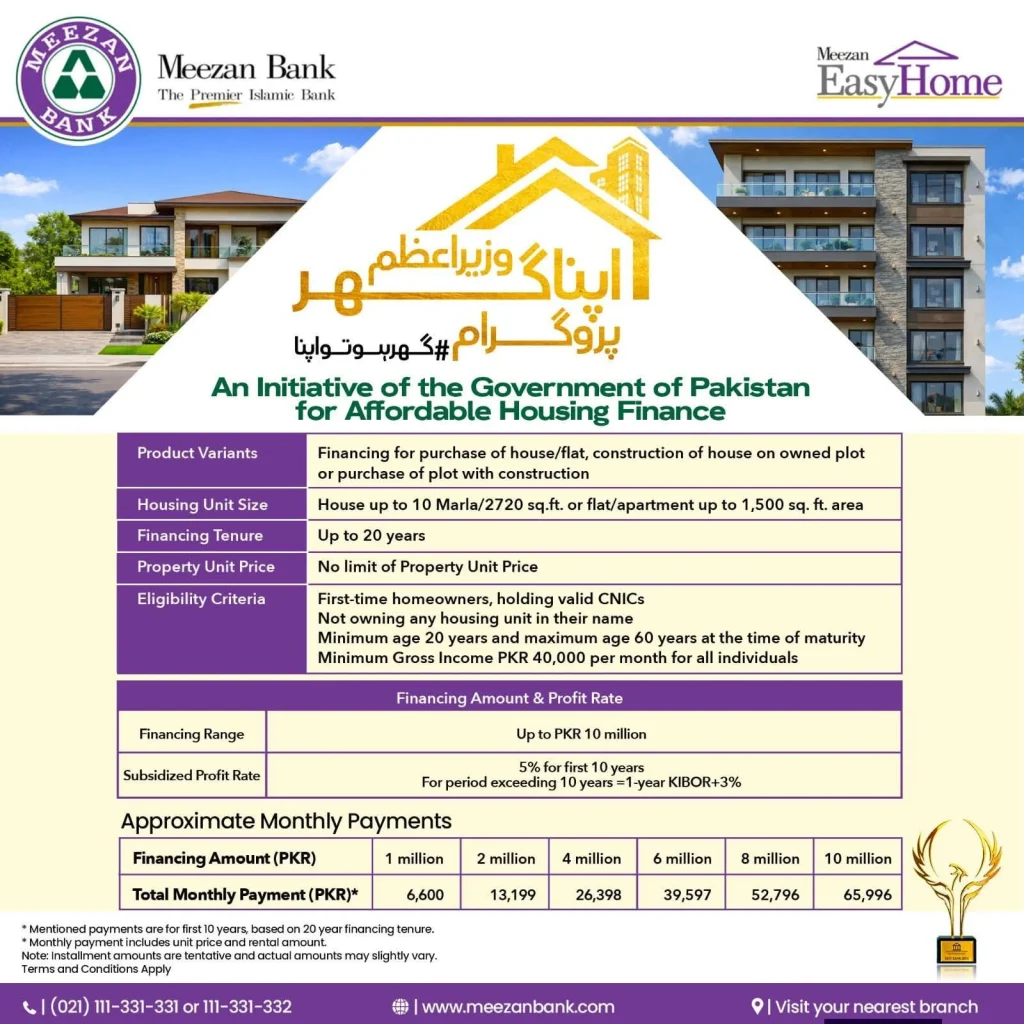

The Meezan Bank Apna Ghar Program 2026, part of a broader national initiative for affordable housing, is designed to bridge the gap between high property prices and the average person’s savings. This Shariah-compliant program offers a realistic way to move into your own home without the burden of traditional high-interest loans.

Why Islamic Housing Finance Matters in 2026

For many Pakistanis, the biggest hurdle to getting a home loan isn’t just the money; it’s the “Riba” or interest. Traditional banking can feel at odds with personal values. This is where Meezan Bank steps in as a leader.

Unlike a conventional loan where you borrow money and pay it back with interest, Meezan Bank operates on the principle of Diminishing Musharakah. In simple terms, the bank and the customer participate in the joint ownership of the property. You pay a monthly amount that includes a “rental” for the bank’s share and a payment to purchase that share. Over time, the bank’s ownership decreases until you own the house 100%.

Key Features of the 10 Million PKR Finance Facility

The 2026 update to the program provides a substantial cushion for middle-income families. While many schemes limit you to very small amounts, this initiative allows you to access up to PKR 10 million.

Flexible Property Options

Whether you want to buy a ready-made house or build one on a piece of land you already own, the program covers it. Here is what you can finance:

- Purchasing a House or Flat: Buy an existing property and move in immediately.

- Construction on Owned Plot: If you already have the land, the bank provides the funds to build the structure.

- Plot Purchase plus Construction: A combined package for those starting from scratch.

Generous Property Sizes

The program recognizes that families need space. You can apply for financing for:

- Houses: Up to 10 Marla (roughly 2720 sq. ft.).

- Apartments/Flats: Up to 1,500 sq. ft. of covered area.

Understanding the Subsidized Profit Rates

The most attractive part of the Meezan Bank Apna Ghar Program is the profit rate. In an era of fluctuating KIBOR rates, the government-backed subsidy provides much-needed stability.

For the first 10 years of your financing, the profit rate is fixed at a low 5%. This is significantly lower than market rates, making the initial decade of homeownership very affordable.

After the first 10 years, the rate transitions to a market-based formula (1-year KIBOR + 3%). Because you will have paid off a large portion of the principal by then, the impact of market changes is much easier to manage.

Detailed Monthly Installment Breakdown

To help you plan your budget, it is essential to look at the numbers. These estimates are based on a 20-year tenure.

| Finance Amount | Estimated Monthly Payment (First 10 Years) |

|---|---|

| PKR 1 Million | Rs. 6,600 |

| PKR 2 Million | Rs. 13,199 |

| PKR 4 Million | Rs. 26,398 |

| PKR 6 Million | Rs. 39,597 |

| PKR 8 Million | Rs. 52,796 |

| PKR 10 Million | Rs. 65,996 |

Note: These amounts are tentative and include both the rental component and the unit price repayment.

Are You Eligible?

Before heading to the bank, check if you meet these fundamental requirements. The program is specifically designed for “first-time homeowners.” This means if you already own a house in your name, you might not qualify for this specific subsidized rate.

1. Age Requirements

You must be at least 20 years old to apply. The maximum age limit is 60 years at the time the financing matures. If you are 45 now, you can comfortably take a 15-year plan.

2. Income Threshold

To ensure that families can comfortably afford the installments, there is a minimum gross income requirement of PKR 40,000 per month. This can be your individual income or a combined income if you are applying with a co-applicant (like a spouse).

3. Documentation

A valid CNIC is mandatory. You will also need to provide proof of income, such as salary slips or business bank statements, to show you can manage the monthly payments.

Meezan Bank Apna Ghar Program 2026

Step-by-Step Application Process

The process is designed to be transparent. Here is how you can get started:

- Initial Assessment: Visit a Meezan Bank branch or use their online portal to check your basic eligibility based on your income.

- Property Selection: Identify the property you wish to buy or the plot you want to build on. Ensure the property has clear legal titles.

- Application Submission: Submit the formal application along with the required processing fees and documents.

- Property Valuation: The bank will conduct a professional valuation and legal check on the property to ensure your investment is safe.

- Approval and Signing: Once approved, you will sign the Musharakah agreement, and the bank will disburse the funds to the seller or contractor.

The Long-term Benefits of 20-Year Tenure

Choosing a 20-year tenure is a smart move for many. While it sounds like a long time, it brings the monthly installment down to a level that is often lower than what you would pay in rent for the same house.

In Pakistan’s economy, the value of money changes over time. An installment of Rs. 26,000 might feel like a lot today, but in five or ten years, as your income grows, that fixed payment becomes a very small percentage of your budget. Meanwhile, the value of your house is likely to increase significantly.

Common Myths About Islamic Housing Finance

Myth 1: It is more expensive than regular loans.

Actually, with the government subsidy, the 5% rate is one of the lowest available in the financial market. Even without the subsidy, the transparent nature of Islamic banking often saves customers from hidden “compounding interest” traps.

Myth 2: The bank owns your house.

The bank is a partner. You have full usage rights and the freedom to live in the house as your own. As you pay your installments, your “share” in the partnership grows until the bank is no longer part of the title.

Final Thoughts for 2026

The real estate market in Pakistan is changing. With the government’s focus on affordable housing, programs like Meezan Bank’s Easy Home are the best way for the salaried class to build equity. Instead of giving your hard-earned money to a landlord every month, you can start building a legacy for your children.

If you meet the income criteria and have been waiting for the right moment, 2026 is the year to take the leap. Visit your nearest Meezan Bank branch to get a personalized quote and see exactly how close you are to owning your dream home.

Frequently Asked Questions (FAQs)

1. Can I pay off the finance earlier than 20 years?

Yes, you can make early payments to purchase the bank’s shares faster. However, it is best to check with your branch regarding any processing terms for early settlement.

2. Is this program only for new houses?

No, you can use this financing to buy an existing house, provided it meets the bank’s legal and structural criteria. You can also use it for the renovation or construction of a house.

3. What if I am a businessman and don’t have a salary slip?

Business owners are eligible! You will need to provide your business registration documents and at least 6 to 12 months of bank statements to prove your monthly income exceeds the PKR 40,000 requirement.

4. Does the “First-time homeowner” rule apply to my spouse too?

Generally, the program aims to help families who do not own a home. If your spouse owns a residential property, it may affect your eligibility for the subsidized government rates. It is always best to declare all assets during the initial consultation.

5. What happens after the first 10 years?

The 5% subsidized rate ends after Year 10. From Year 11 to Year 20, the rate will be based on the prevailing 1-year KIBOR plus a 3% margin. This ensures the bank can continue to manage the facility according to current economic conditions.