If you are a government employee in Pakistan, your General Provident (GP) Fund is more than just a deduction on your monthly pay slip. It is a financial safety net, a saving for your retirement, and a source of support when life throws unexpected expenses your way.

As we move through 2026, the rules for applying for an advance (a loan from your own savings) have become more streamlined. However, understanding the difference between refundable and non-refundable advances, and knowing how to use the PIFRA system effectively, is essential for every “Sarkari” employee.

In this guide, we will break down the latest rules, the application steps, and how you can check your current balance from the comfort of your home.

What is the GP Fund?

The General Provident Fund is a compulsory savings scheme for government employees. Every month, a specific portion of your salary is deducted and kept in this fund. The government manages this money and adds a “markup” or interest rate to it every year.

By the time you retire, this fund usually grows into a significant amount. However, the government allows you to take a “loan” or an “advance” from this fund while you are still in service for specific needs like weddings, education, or house construction.

GP Fund Advance Rules for 2026

The Finance Division has updated certain protocols to ensure that funds are released more quickly and that the process is transparent. There are two main types of advances you can take.

1. Refundable GP Fund Advance

This is a temporary loan. You take the money, use it, and then pay it back to the government in easy monthly installments.

- Eligibility: You can apply for this even early in your career.

- Repayment: Usually, the amount is paid back in 24 to 36 installments, which are deducted directly from your salary.

- Limit: Typically, you can draw up to 80% of the balance available in your account, though this depends on the specific department’s policy.

2. Non-Refundable GP Fund Advance

This is the preferred choice for senior employees. You take the money, and you never have to pay it back. It is treated as a final withdrawal from your total balance.

- Age Requirement: Under the 2026 rules, employees who have reached the age of 50 (in some provinces, it is 45) are eligible for a non-refundable advance.

- No Deductions: Since it is non-refundable, your monthly salary remains the same; no installments are deducted.

- Usage: This is usually granted for major life events like a daughter’s marriage, building a house, or performing Hajj.

Valid Reasons for Applying for an Advance

You cannot just withdraw GP Fund money for no reason. The AG (Accountant General) office requires a valid justification. Common reasons accepted in 2026 include:

- Medical Expenses: If you or a family member needs urgent hospital treatment.

- Education: Paying for a child’s university fees or professional courses.

- Marriage: Covering the wedding costs of children or dependent siblings.

- Housing: Buying land, building a new house, or making major repairs to your current home.

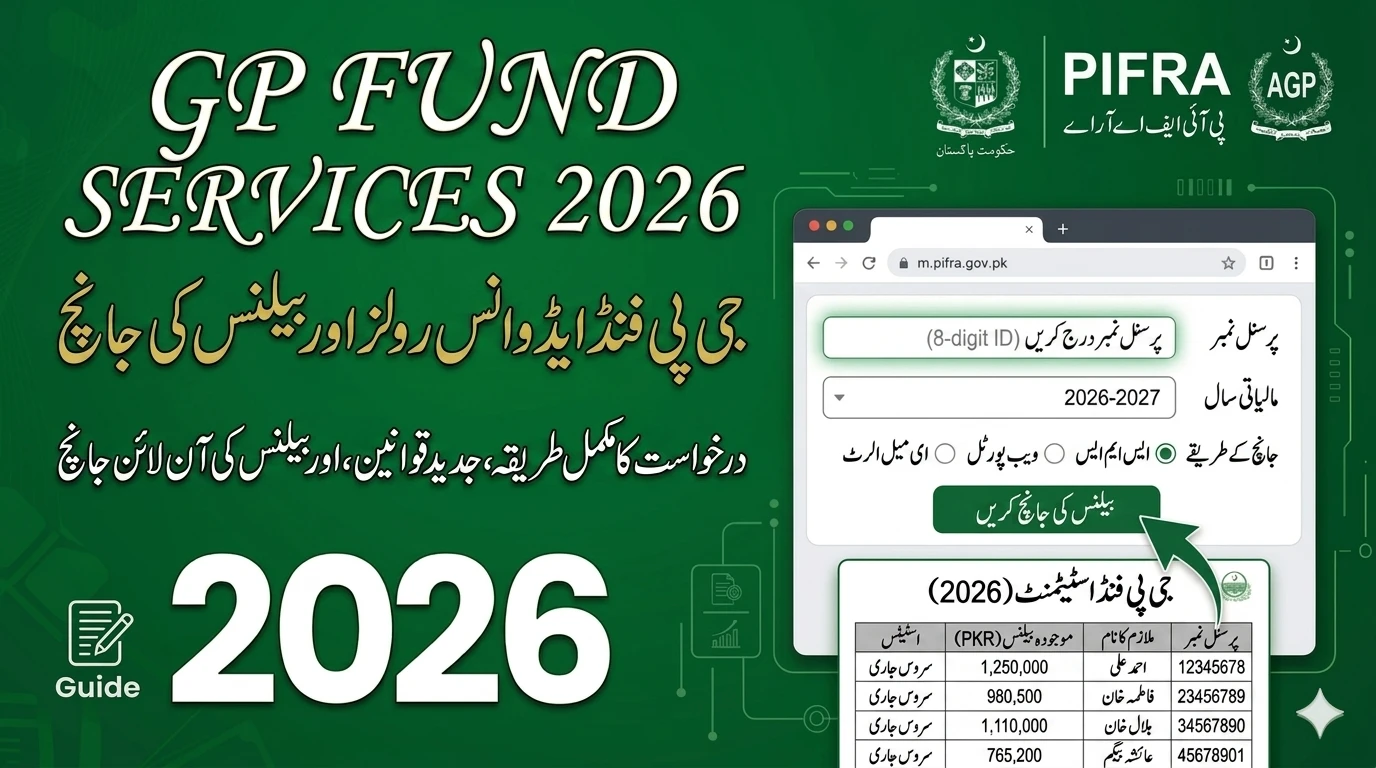

How to Check Your GP Fund Balance via PIFRA

Gone are the days when you had to visit the District Accounts Office (DAO) and stand in long lines just to know how much money you had. The PIFRA (Project for Improvement of Financial Reporting and Auditing) system has made it incredibly easy.

Method 1: The Monthly Salary Slip

If you have registered your email with PIFRA, you receive a digital salary slip every month.

- Open your latest salary slip email.

- Look at the bottom section or the “Deductions” column.

- You will see a heading for GP Fund Balance. It shows the opening balance for the year and the total contributions made so far.

Method 2: PIFRA SMS Service

In 2026, the SMS service is more active than ever.

- Send your CNIC number and Personal Number to the official PIFRA shortcode (check with your department for the current 2026 active number).

- You will receive an instant reply with your current fund balance.

Method 3: The PIFRA Web Portal

You can also visit the official PIFRA or the relevant provincial Accountant General website. By entering your personal number and date of birth, you can generate a “GP Fund Ledger,” which shows every single deduction made throughout your career.

Step-by-Step Guide to Applying for a GP Fund Advance

If you have decided that you need to take an advance, follow these steps to ensure your application isn’t rejected.

Step 1: Obtain the Application Form

You can get the GP Fund Advance Form (Form-TR-22) from your office’s establishment branch or download it from the AG Punjab, Sindh, KPK, or Balochistan website.

Step 2: Fill in Your Details

You will need to provide:

- Your Name, Designation, and BPS (Pay Scale).

- Your Personal Number (8-digit ID).

- The specific amount you want to withdraw.

- The reason for the advance (attach supporting documents like a wedding card or medical bill).

Step 3: Verification by the DDO

Your Drawing and Disbursing Officer (DDO) must verify that you are a regular employee and that your reason is genuine. They will sign and stamp your application.

Step 4: Submission to the AG Office/DAO

Once signed by your department head, the file goes to the District Accounts Office or the Accountant General’s office. They will check your total balance in the SAP system to ensure you have enough funds.

Step 5: Issuance of the Sanction Order

If everything is in order, the AG office will issue a “Sanction Order.” This is the official approval.

Step 6: Payment Credit

Once the sanction is processed, the money is usually transferred directly into your bank account along with your next salary, or as a separate “supplementary bill.”

Latest Updates for 2026: Markup Rates

Every year, the Finance Division announces the interest (markup) rate for the GP Fund. For the fiscal year 2025-2026, the rates have been adjusted to match the current economic conditions.

- Interest-Free Option: Remember, if you do not want to receive interest for religious reasons, you can submit a simple application to your DAO to make your GP Fund “Interest-Free.” This is a common practice for many employees in Pakistan.

Common Reasons for Rejection (And How to Avoid Them)

Many employees face delays because of simple mistakes. Keep an eye on these:

- Wrong Personal Number: Ensure your 8-digit ID matches your salary slip.

- Missing Installment History: If you are applying for a second refundable advance before paying back the first one, your application might be rejected.

- Incomplete Documents: If you say you need money for a house, you must show proof of ownership or a construction estimate.

- Signature Mismatch: Ensure your signature matches the one in the government records.

Tips for a Faster Approval

- Check your Balance First: Never ask for more money than what is available in your account. Use the PIFRA portal to see your exact balance before filling the form.

- Keep Copies: Always keep a photocopy of the signed application before submitting it to the AG office.

- Follow Up: After a week of submission, visit the DAO or check your status online to see if any “objections” have been raised.

FAQs

1. Can I take a GP Fund advance more than once?

Yes, for refundable advances. However, you usually need to have paid back a certain percentage of your previous loan before you can apply for a new one.

2. Is there any fee for checking the balance on PIFRA?

No, the online portal and email services are completely free. However, standard network charges may apply if you use the SMS service.

3. How long does the approval process take?

Usually, it takes 10 to 15 working days from the date of submission to the AG office, provided there are no objections in your file.

4. What happens to my GP Fund if I am transferred?

Your GP Fund balance is linked to your Personal Number. When you move to a new district or department, your “History of Services” and fund balance are transferred electronically in the PIFRA system.

5. Can I withdraw my entire GP Fund before retirement?

Generally, no. You can only take advances (up to 80% or 90% in some cases). The full and final payment is only made at the time of retirement or in the case of the employee’s death (paid to the family).

Conclusion

Understanding the GP Fund Advance Rules 2026 is vital for your financial planning. Whether you are using the PIFRA balance check service or preparing an application for a non-refundable advance, staying informed helps you avoid unnecessary stress.

The system is designed to help you. By following the correct steps and keeping your digital records updated, you can ensure that your hard-earned savings are available to you exactly when you need them most.

یہ آرٹیکل 2026 میں پاکستان کے سرکاری ملازمین کے لیے جی پی فنڈ (GP Fund) ایڈوانس رولز کی مکمل اور جامع وضاحت فراہم کرتا ہے۔ اس تحریر میں ریفنڈ ایبل (قابلِ واپسی) اور نان ریفنڈ ایبل (غیر واپسی) ایڈوانس کے درمیان فرق، اہلیت کے نئے معیار، اور درخواست دینے کے مکمل ڈیجیٹل طریقے کو آسان زبان میں سمجھایا گیا ہے۔

آرٹیکل کا ایک اہم حصہ PIFRA سسٹم کے ذریعے گھر بیٹھے جی پی فنڈ بیلنس چیک کرنے کے مختلف طریقوں، جیسے کہ ای میل، ایس ایم ایس اور آن لائن ویب پورٹل کے استعمال پر مبنی ہے۔ اس کے علاوہ، اس میں فارم TR-22 کو بھرنے، DDO سے تصدیق کروانے، اور اکاؤنٹنٹ جنرل (AG) آفس سے منظوری حاصل کرنے کا مرحلہ وار طریقہ کار بھی شامل کیا گیا ہے۔

اگر آپ اپنی بیٹی کی شادی، بچوں کی تعلیم، گھر کی تعمیر یا کسی طبی ضرورت کے لیے اپنے فنڈز سے فائدہ اٹھانا چاہتے ہیں، تو یہ گائیڈ آپ کی تمام مالیاتی الجھنوں کو دور کرنے اور بروقت رقم کے حصول میں مددگار ثابت ہوگی۔ یہ خاص طور پر ان ملازمین کے لیے تیار کیا گیا ہے جو دفتروں کے چکر لگائے بغیر اپنے حقوق سے آگاہ ہونا چاہتے ہیں۔