For most families in Pakistan, the biggest hurdle to owning a home isn’t the desire—it’s the financing. We all want a place to call our own, but the math behind bank loans can feel like a puzzle. You might find yourself asking: “If I earn 60,000 PKR, can I actually afford a house loan?” or “How much will the bank take from my salary every month?”

The House Building Finance Company (HBFC) has been helping Pakistanis answer these questions for decades. Their Mera Ghar Mera Ashiana Scheme is specifically designed for people with fixed monthly incomes.

In this guide, we will break down exactly how your salary connects to your loan amount. We will also look at the monthly installments for different timeframes so you can plan your future with confidence.

Why Does Your Salary Matter for a House Loan?

When you walk into a branch for a loan, the first thing the officer asks for is your salary slip. This isn’t just about how much you earn; it’s about your “repayment capacity.”

HBFC needs to make sure that after you pay your monthly installment, you still have enough money left for groceries, electricity bills, and your children’s school fees. They generally follow a “debt-to-burden” ratio. Usually, they don’t want your total loan payments to exceed 40% to 50% of your net income.

Net Salary vs. Gross Salary

It is important to look at your Net Salary—the amount that actually hits your bank account after taxes. This is the figure HBFC uses to decide if you are a safe bet for a 10 or 20-year commitment.

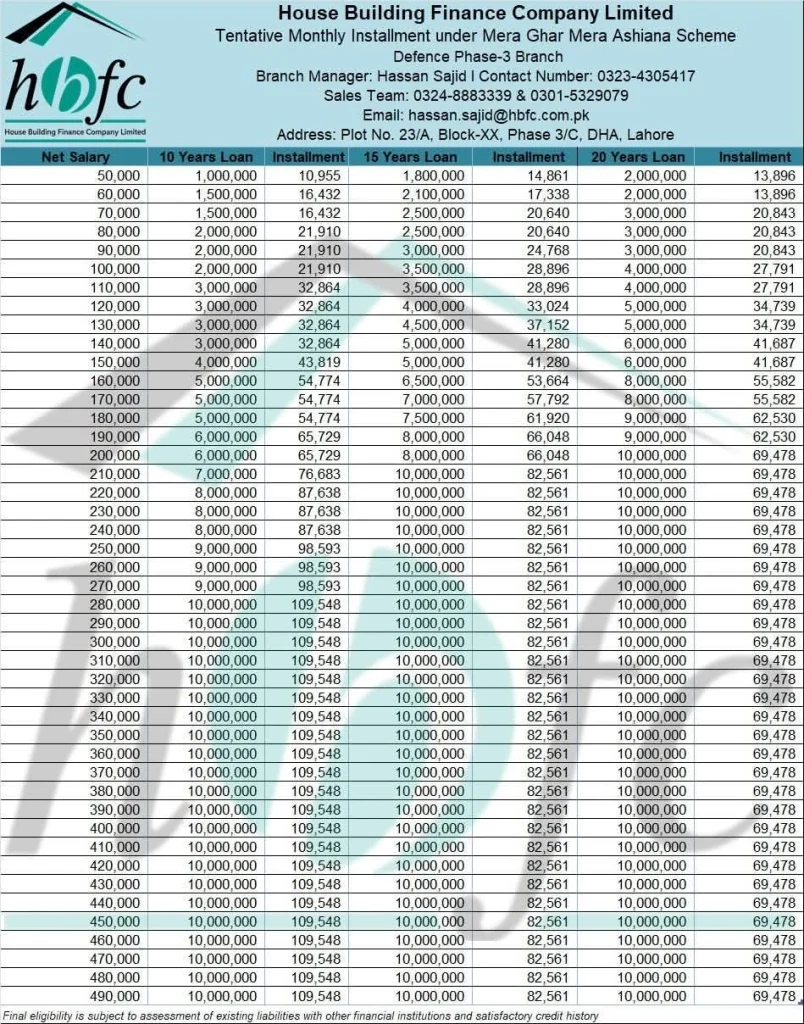

The HBFC Installment Table: A Closer Look

HBFC has a structured table that matches your income to a specific loan limit. Let’s look at how these numbers work in the real world for the year 2026.

For Low-to-Mid Income Earners (PKR 50,000 – 100,000)

If your monthly take-home pay is in this bracket, you are likely looking for an entry-level home or a small apartment.

- Salary of 50,000 PKR: You can typically secure a loan between 1 and 2 million PKR. Over 20 years, your installment would be roughly 13,896 PKR.

- Salary of 80,000 PKR: Your eligibility increases. You could get up to 3 million PKR. A 15-year plan for this amount would cost you about 20,640 PKR per month.

For Established Professionals (PKR 150,000 – 250,000)

This bracket allows you to look at larger properties or better locations in cities like Lahore, Karachi, or Islamabad.

- Salary of 150,000 PKR: You could qualify for a 6 million PKR loan. On a 20-year plan, the monthly payment is approximately 41,687 PKR.

- Salary of 250,000 PKR: At this level, you hit the higher end of the scheme, qualifying for up to 10 million PKR.

[Image suggestion: A simple bar chart showing how the loan amount grows as the salary increases]

Choosing Your Tenure: 10, 15, or 20 Years?

One of the biggest decisions you will make is how long you want to keep paying the bank. HBFC offers three main “tenures.” Each has its own pros and cons.

1. The 10-Year Plan (Short & Sweet)

This is for people who want to be debt-free quickly.

- The Good: You pay much less in total interest to the bank. You own your home fully in just a decade.

- The Bad: The monthly installments are very high. For a 10 million PKR loan, you’d be paying nearly 110,000 PKR a month. This requires a very high salary to stay comfortable.

2. The 15-Year Plan (The Middle Path)

Many families choose this because it balances the monthly cost with the total interest. It’s a great “safety first” option.

3. The 20-Year Plan (Maximum Affordability)

This plan is designed to give you the most money for the lowest monthly cost.

- The Good: It allows you to get a bigger house today. The installments are the lowest they can be.

- The Bad: You end up paying more interest over the long run because you are borrowing the money for a longer time.

Three Things That Can Stop Your Loan Approval

Even if your salary is high, there are “invisible” factors that HBFC looks at before saying yes. Knowing these beforehand can save you a lot of time.

Your Credit History (The CIB Report)

The State Bank of Pakistan keeps a record of every time you took a loan or used a credit card. If you were late on payments in the past, your “CIB report” will show it. A bad report is the fastest way to get a loan rejected. Always pay your small bills on time to keep this record clean.

Existing Monthly Deductions

Do you already have a car loan? Are you paying off a mobile phone on installments? HBFC will subtract those monthly payments from your salary before they decide how much more you can afford. If you have too many small loans, you might not get a large house loan.

The Property’s Legal Status

HBFC will only give you money for a “clean” property. This means the house or plot must have a clear Registry, Inteqal, or an NOC (No Objection Certificate) from authorities like DHA, LDA, or CDA. If the property is in a disputed area, the bank will not finance it.

How to Apply: A 4-Step Process

Ready to start? Here is the simple way to get moving with your HBFC application:

- Step 1: Document Check. Get your last 6 months’ bank statements and 3 months’ salary slips ready.

- Step 2: Visit a Branch. Go to your nearest HBFC office (like the Phase 3 DHA branch in Lahore). Ask for a “Tentative Assessment.”

- Step 3: Property Appraisal. Once you find a house, the bank will send an evaluator to check its price and a lawyer to check its papers.

- Step 4: Approval & Disbursement. If everything matches up, the bank will issue the check to the seller, and you get the keys!

Why HBFC is Different from Commercial Banks

Many people ask, “Why not just go to a big commercial bank?” While commercial banks are great, HBFC is a specialized institution. Their only job is housing.

Because of this focus, they often have more experience dealing with low-income brackets and offer schemes like “Mera Ghar Mera Ashiana” that are specifically protected for the common man. They understand the local property market better than a general bank that also sells car insurance and credit cards.

Conclusion

Owning a home shouldn’t be a mystery. By looking at your net salary and comparing it against the 10, 15, and 20-year installment plans, you can find a path that fits your budget.

Don’t wait for “the perfect time” to buy, as property prices usually go up faster than salaries. Use the tables provided, check your CIB status, and take the first step toward your own front door. Your “Ashiana” is closer than you think.

How Much House Loan Can You Get on Your Salary?

Frequently Asked Questions (FAQs)

1. Can I apply with my spouse to increase the loan amount?

Yes! This is called “Co-Borrowing.” If both husband and wife are working, you can combine your salaries. This allows you to qualify for a much higher loan than you could on a single salary.

2. Is there an age limit for HBFC loans?

Yes. Generally, the loan tenure must end before you reach the age of 60 (for salaried individuals) or 65 (for self-employed). So, if you are 50 years old, you might only qualify for a 10-year loan.

3. What is the “Markup” or interest rate?

The rates are usually tied to KIBOR (the market rate set by banks). It is a “variable” rate, meaning if the national profit rates change, your installment might adjust slightly. Always ask the bank for the current “Spread” they are charging over KIBOR.

4. Can I build a house on a plot I already own?

Absolutely. HBFC offers “Construction Loans.” If you already own the land, the bank will give you money in stages (installments) as you complete the foundation, the walls, and the roof.

5. What happens if I lose my job?

This is a serious situation. You should immediately contact HBFC. They often have policies for “Rescheduling” where they might give you a few months of relief or lower your installments temporarily while you find new employment.