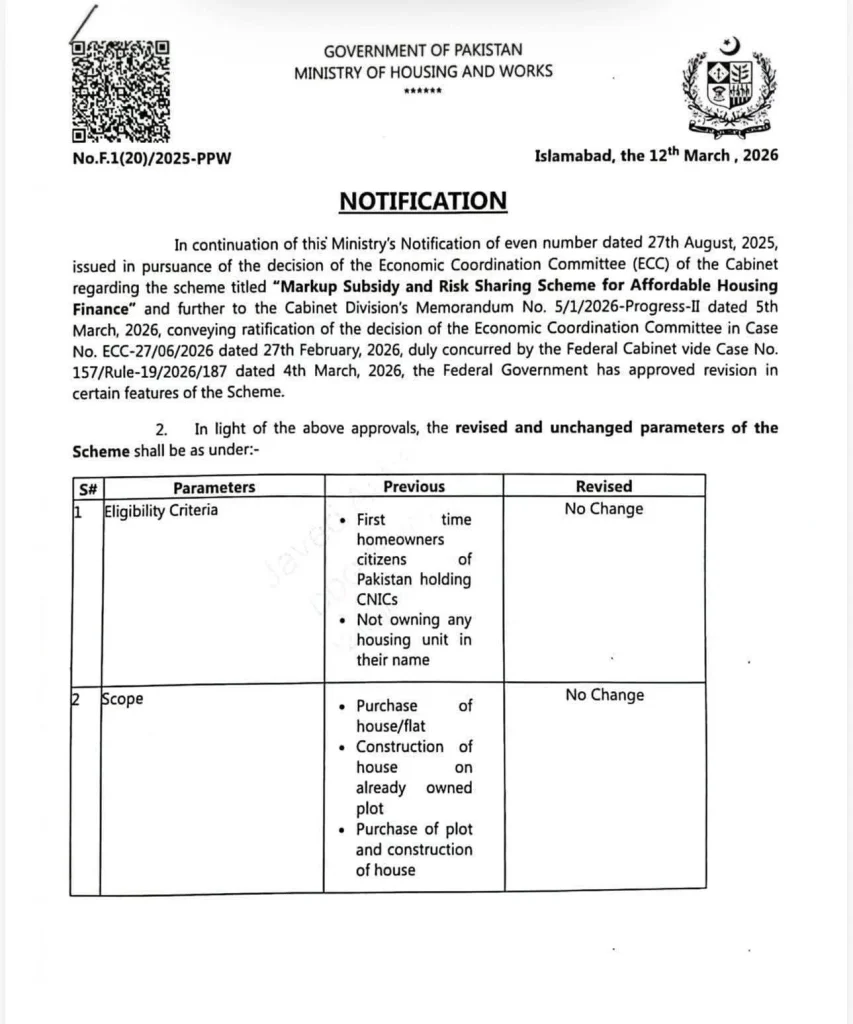

Owning a home is a cornerstone of financial security and personal pride. In Pakistan, the dream of having a personal roof has often been sidelined by rising property prices and high interest rates. However, the Pakistan Housing Finance Scheme 2026 is changing the landscape. With significant revisions to the Markup Subsidy and Risk Sharing Scheme, the government has made it easier for middle- and low-income families to transition from renting to owning.

If you are looking for a reliable way to finance your first home, this guide will walk you through the updated features, eligibility requirements, and the step-by-step application process for this government-backed initiative.

Introduction to Pakistan Housing Finance Scheme 2026

The Ministry of Housing and Works, in collaboration with the State Bank of Pakistan (SBP), has introduced a revamped version of its affordable housing finance program. This initiative is specifically designed to address the housing shortage in the country. By providing subsidized interest rates and risk-sharing guarantees to banks, the government ensures that citizens can access credit that would otherwise be too expensive.

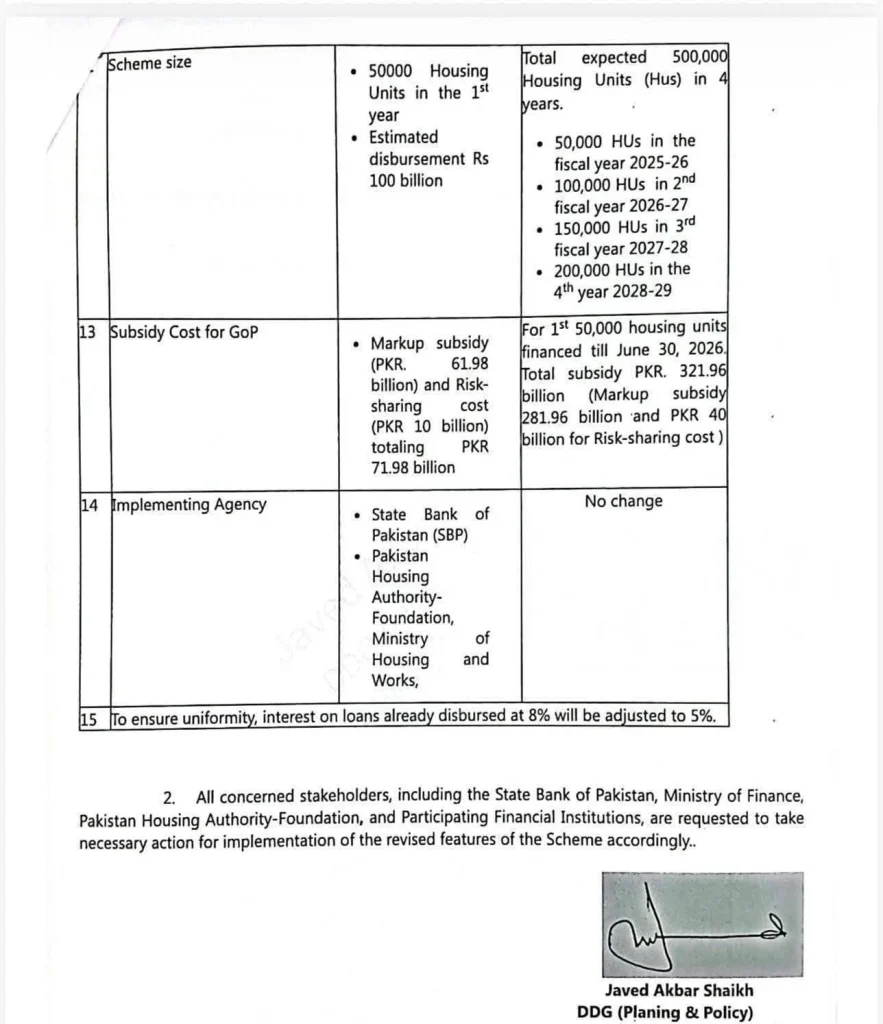

As of March 2026, the scheme has seen a massive expansion. The focus has shifted from providing small, basic units to allowing citizens to purchase or build more substantial family homes. With a target of 500,000 housing units over the next four years, this is currently the most significant financial inclusion project for the Pakistani construction sector.

Who Can Apply for Pakistan Housing Finance Scheme

The scheme is inclusive but targeted. It is built for the “common man”—salaried individuals, self-employed professionals, and small business owners who have a steady income but lack the lump sum capital to buy property upfront.

The primary focus is on first-time homeowners. If you already own a residential property in your name, you are generally not the target audience for this specific subsidy. The goal is to help those who are currently living in rented spaces or joint family systems to establish their own independent households.

Whether you are a young professional starting your career or a head of a household looking for a permanent residence for your children, this scheme provides a structured path to homeownership.

Eligibility Criteria

To maintain transparency and ensure the benefits reach the right people, the government has set specific eligibility benchmarks. These criteria are straightforward but must be met before a bank can process your application.

1. Citizenship and Identity

Every applicant must be a citizen of Pakistan. You must possess a valid Computerized National Identity Card (CNIC). For overseas Pakistanis, specific bank policies might apply, but the core scheme is focused on resident citizens.

2. Property Ownership Status

You must be a first-time homeowner. This means that at the time of application, you should not own any other housing unit in your name. Banks often require an affidavit or a verification check to confirm this status.

3. Creditworthiness

While the government subsidizes the loan, the money is disbursed by commercial banks. Therefore, you must have a clean credit history. If you have defaulted on previous bank loans or credit cards, your application may face hurdles.

4. Income Requirements

You need to show a consistent source of income. This can be verified through:

- Salary slips and employment letters for salaried individuals.

- Bank statements and tax returns for business owners or freelancers.

- Rental income or other verifiable cash flows.

Pakistan Housing Finance Scheme 2026

How to Apply for Government Home Loan

The application process has been streamlined to avoid the “red tape” usually associated with government programs. Since multiple commercial and Islamic banks are participating, you can apply at a branch near you.

Step 1: Research and Choose a Bank

Almost all major banks in Pakistan, including HBFC (House Building Finance Company), are part of this network. Compare the customer service and proximity of different banks to choose the one that suits you best.

Step 2: Initial Consultation

Visit the dedicated “Housing Finance” desk at your chosen bank. Explain that you wish to apply under the Government Markup Subsidy Scheme (G-MSS). The bank officer will provide you with a specific application form.

Step 3: Document Preparation

Gather all necessary legal and financial documents. This is the most crucial part of the process. If your documents are incomplete, the processing time will increase significantly.

Step 4: Property Selection and Valuation

If you are buying a constructed house or a flat, the bank will conduct a professional valuation of the property. For those building on their own plot, the bank will review the construction plan and maps.

Step 5: Approval and Disbursement

Once the bank is satisfied with your income and the property’s legal status, they will issue an offer letter. After you accept the terms and pay your 10% equity share, the funds will be disbursed directly to the seller or released in stages for construction.

Benefits of Pakistan Housing Finance Scheme

The 2026 revisions have introduced several perks that make this scheme far superior to standard commercial home loans.

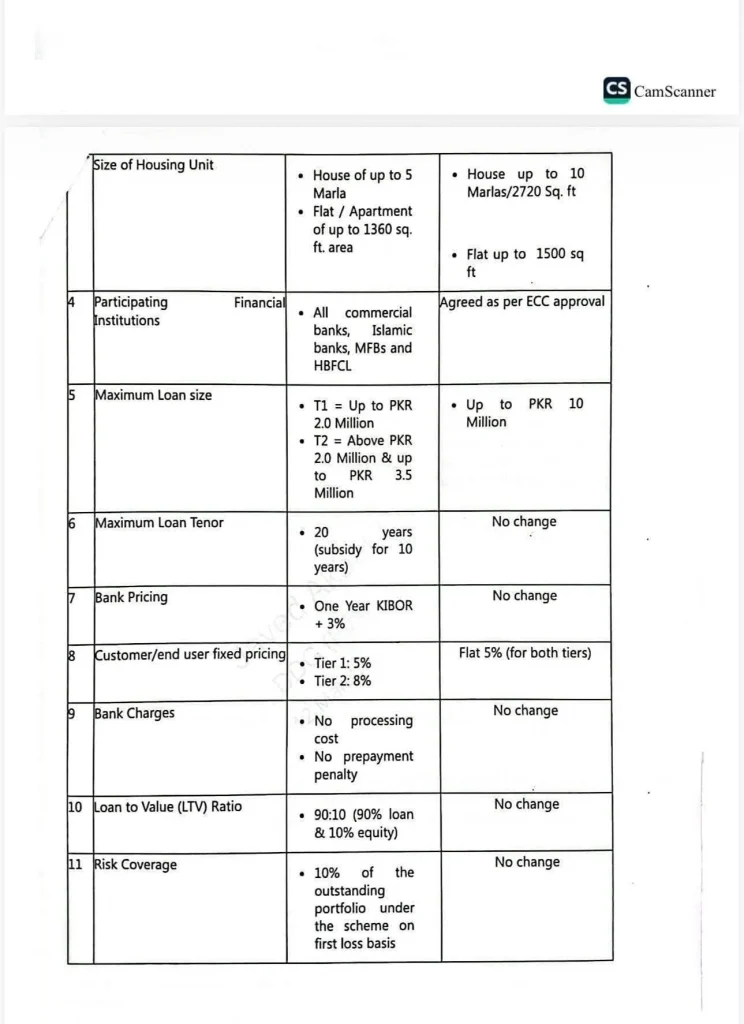

Increased Loan Limits

The maximum loan size has been increased to PKR 10 million (1 Crore). Previously, limits were restricted to 2.0 or 3.5 million, which was often insufficient for urban centers like Lahore, Karachi, or Islamabad.

Uniform Low Interest Rates

The most significant benefit is the Flat 5% Markup. In an environment where market interest rates (KIBOR) can be quite high, paying only 5% is a massive relief. This rate applies to both Tier 1 and Tier 2 categories, ensuring everyone pays the same low rate.

Larger Property Sizes

You can now use this loan to build or buy a house up to 10 Marla (2720 Sq. ft). This is a major upgrade from the previous 5-marla limit, allowing for larger, more comfortable family homes.

Financial Incentives

- No Processing Fees: Banks are instructed not to charge heavy processing costs.

- No Prepayment Penalty: If you receive a bonus or extra savings and want to pay off your loan early, the bank will not fine you.

- Long Tenor: You have up to 20 years to repay, keeping your monthly installments manageable.

| Parameter | Previous Feature | New Revised Feature (2026) |

|---|---|---|

| Max Loan Amount | Up to PKR 3.5 Million | Up to PKR 10 Million |

| Interest Rate (Markup) | 5% to 8% | Flat 5% for everyone |

| House Size | Up to 5 Marla | Up to 10 Marla |

| Flat Size | Up to 1360 Sq. ft | Up to 1500 Sq. ft |

| Repayment Period | 20 Years | 20 Years |

Required Documents

To speed up your application, keep the following documents ready:

- Identity: Copy of valid CNIC (Applicant and Co-applicant).

- Photos: 2 Passport-sized photographs.

- Income Proof: * Salary slips for the last 3 months.

- Bank statements for the last 6 to 12 months.

- Employer certificate.

- Business Docs: For self-employed individuals, a copy of the NTN and tax returns for 2 years.

- Property Docs: * Copy of the Title Deed (Allotment letter/Transfer letter).

- Approved building plan (if constructing).

- Non-Encumbrance Certificate (NEC).

FAQs

Q1: Can two brothers or a husband and wife apply together?

Yes. You can have a co-applicant. This is often recommended because combining two incomes can help you qualify for a higher loan amount.

Q2: What is the 90:10 LTV ratio?

LTV stands for “Loan to Value.” It means the bank will provide 90% of the property’s value as a loan, and you must provide the remaining 10% as your own equity (down payment).

Q3: Is this scheme available for Islamic Banking?

Yes. All major Islamic banks in Pakistan offer this scheme under Shariah-compliant modes of financing like “Diminishing Musharakah.”

Q4: What happens if I already have an 8% markup loan?

The new government notification states that loans already disbursed at 8% will be adjusted down to 5% to ensure uniformity and fairness for all borrowers.

Q5: Can I buy a plot with this loan?

The loan can be used for “Purchase of plot and construction of house.” You cannot buy a plot and leave it vacant; the ultimate goal must be the construction of a residence.

Conclusion

The Pakistan Housing Finance Scheme 2026 is more than just a financial product; it is a bridge to a better quality of life. By increasing loan limits to PKR 10 million and slashing interest rates to a flat 5%, the government has removed the biggest barriers to homeownership.

If you are a first-time buyer, there has never been a better time to invest in your future. Gather your documents, visit your nearest bank, and start the journey toward owning your home today.