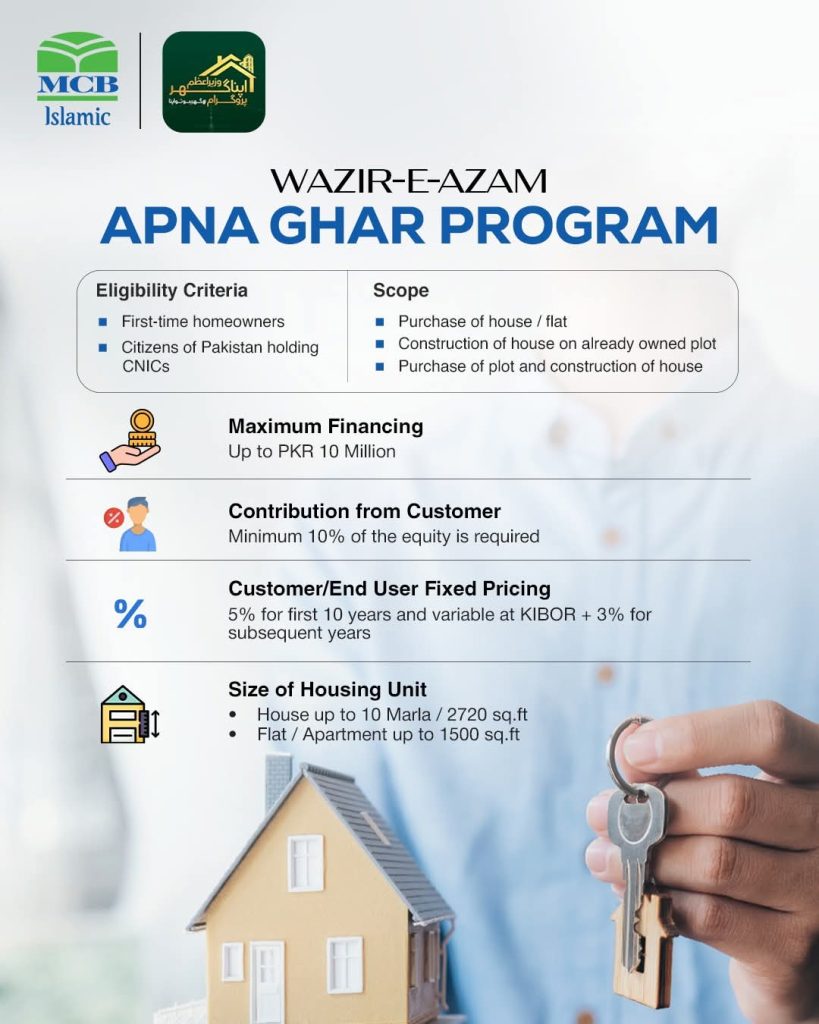

Buying a home is probably the biggest dream for any Pakistani family. For years, the barrier has always been the same: skyrocketing property prices and high interest rates. However, the Wazir-e-Azam Apna Ghar Program, specifically through MCB Islamic, is changing the game for 2026.

If you are tired of paying rent and want a roof you can truly call your own, this program might be your best shot. Let’s break down everything you need to know without the confusing financial jargon.

What Makes This Program Different in 2026?

Most bank loans feel like a trap because of fluctuating interest rates. You start paying one amount, and two years later, your monthly installment doubles. The Wazir-e-Azam Apna Ghar Program is designed to be “pro-people.”

By partnering with MCB Islamic, the government has ensured that the financing follows Shariah-compliant principles. This means you aren’t just taking a “loan”—you are entering into a partnership with the bank to eventually own your home.

The Financial Breakdown: What Can You Get?

The numbers here are quite impressive compared to standard commercial loans. The program is tailored for the common man who needs a significant boost to enter the real estate market.

1. Maximum Financing Limit

You can get up to PKR 10 Million (1 Crore). This is a substantial amount that covers a decent 5 to 10 Marla house in most cities or a high-end apartment in urban centers like Lahore, Karachi, or Islamabad.

2. The 5% Fixed Rate Hook

This is the “star feature” of the scheme. For the first 10 years, your pricing is fixed at 5%. In a world where inflation is unpredictable, having a locked-in rate for a decade provides incredible peace of mind. After those 10 years, the rate shifts to a variable KIBOR + 3% model.

3. Your Contribution (The Down Payment)

You don’t need to have half the money saved up. The bank only asks for a minimum of 10% equity. If you are looking at a house worth 10 million PKR, you only need to bring 1 million PKR to the table. The bank handles the rest.

Are You Eligible? Let’s Check.

The government wants to ensure this money goes to those who actually need it, rather than wealthy investors. Because of this, the criteria are very specific:

- First-Time Homeowners Only: If you already own a house registered in your name, you cannot apply. This scheme is strictly for those moving from a rental or a shared family home to their first independent property.

- Pakistani Citizenship: You must hold a valid CNIC.

- Income Stability: While the program is flexible, you still need to show you can afford the monthly installments. Both salaried and self-employed individuals can apply.

What Kind of Property Can You Buy?

You aren’t restricted to just one type of building. The “Scope” of the program is quite broad to fit different lifestyle needs:

Houses and Flats

Whether you want a standalone house in a housing society or a modern flat in a high-rise, both are covered.

- Size Limits for Houses: Up to 10 Marla or 2720 square feet.

- Size Limits for Flats: Up to 1500 square feet.

Construction on Owned Land

Maybe you already inherited a plot or bought one years ago but never had the cash to build. This program allows you to get financing specifically for the construction phase.

Plot + Construction

If you have found the perfect piece of land but don’t have the money for the plot or the bricks, you can apply for a combined package. The bank will help you buy the land and then provide funds for the building process.

Why Choose the Islamic Path (MCB Islamic)?

Since the user is looking for a “Smarter Workflow,” it’s important to understand the “Why.” MCB Islamic uses a model called Diminishing Musharakah.

Instead of lending you money and charging interest (Riba), the bank buys the property with you. You stay in the house and pay “rent” for the bank’s share while slowly buying out the bank’s units of ownership. Once you’ve bought all the units, the house title transfers entirely to you. It is transparent, ethical, and fits the values of many Pakistani households.

The Step-by-Step Application Process

Don’t let the paperwork scare you. Here is the simplified path to getting your keys:

Step 1: Document Gathering

You will need your CNIC, proof of income (salary slips or business bank statements), and the details of the property you intend to buy. If you are building, you’ll need the approved map and a cost estimate.

Step 2: Initial Assessment

Visit an MCB Islamic branch. They will check your “repayment capacity.” They look at your monthly income versus your expenses to make sure the 5% installment won’t burden your family.

Step 3: Property Valuation

The bank will send an expert to the house or plot you’ve chosen. They need to verify that the property is actually worth the price you are paying and that the legal titles are “clean” (no litigation).

Step 4: Approval and Transfer

Once the bank is satisfied, they will provide the 90% financing. You pay your 10%, the legal documents are signed, and you can start moving your furniture in!

Pro-Tips for a Successful Application

- Clean Your Credit History: Ensure you have no outstanding defaults on credit cards or other bank loans.

- Verify the Property Documents: Before even going to the bank, ask the seller for the “Allotment Letter” or “Transfer Letter.” If the property isn’t legal, the bank won’t fund it.

- Joint Income: If your individual salary is low, you can often add a co-applicant (like a spouse or parent) to increase your total “eligible income.”

Final Thoughts

The Wazir-e-Azam Apna Ghar Program via MCB Islamic is more than just a financial product; it’s a social safety net. In 2026, as the real estate market continues to evolve, locking in a 5% rate for ten years is one of the smartest financial moves a young professional or a small business owner can make.

Stop paying someone else’s mortgage through rent. Start building your own equity today.

Wazir-e-Azam Apna Ghar Program (2026)

Frequently Asked Questions (FAQs)

1. Can I sell the house before the 10 years are up?

Yes, but you will need to settle the remaining balance with MCB Islamic first. There may be specific terms regarding early settlement in the Shariah-compliant contract, so always read the fine print.

2. Is there an age limit for applicants?

Generally, you must be between 25 and 60 years old at the time of the financing’s maturity. This ensures that the applicant is within their “working years” to comfortably pay back the bank.

3. What happens after the first 10 years?

After the 10th year, the “subsidized” rate ends. Your pricing will then be based on the KIBOR (Karachi Interbank Offered Rate) plus a 3% margin. This is the standard market rate.

4. Can I apply if I live abroad (Overseas Pakistani)?

Yes! Overseas Pakistanis are often encouraged to invest in these schemes, provided they can prove their foreign income and provide the necessary documentation through the Roshan Digital Account or similar channels.

5. Are there any hidden charges?

While the 5% rate is clear, you should budget for “processing fees,” “legal documentation fees,” and “property valuation charges.” These are standard one-time costs at the beginning of the process.